- Research Member

Professor Yishay Yafeh

Biography

Yishay Yafeh holds a Ph.D. in Economics from Harvard University (1993), and has taught at Oxford, Montreal and the Hebrew University. He has served Vice Dean (2010-2012) and Dean (2012-2016) of the School of Business Administration of the Hebrew University. His research interests are financial systems and financial intermediation, the economies of East Asia, and economic and financial history. In the past, Yishay served as advisor to the Bank of Israel, the Israel Securities Authority, and the International Monetary Fund. His research has been published, among others, in the Journal of Finance, the Quarterly Journal of Economics, the Journal of Economic Literature, the Journal of Business and the Review of Finance. He co-authored, together with Paolo Mauro and Nathan Sussman, the book Emerging Markets and Financial Globalization (Oxford University Press, 2006).

Current Projects

Eugene Kandel, Konstantin Kosenko, Randall Morck and Yishay Yafeh

Abstract

Pyramidal business groups are prominent in most countries, but virtually absent in the United States today. Newly-assembled data show that, until the middle of the twentieth century, groups dominated the US economy as well. We relate their demise to a barrage of New Deal regulatory reforms. Of these, the Public Utility Holding Company Act, inter-corporate dividend taxation and (to a lesser extent) the Investment Companies Act took direct aim at pyramids. Enhanced investor protection and estate taxes may have also contributed; and banking reforms likely affected the few groups that contained banks. Antitrust enforcement was not (directly) linked to the process. We conclude that sustained regulatory pressure on multiple fronts, supported by an anti-big business climate, precipitated the dissolution of US groups.

Incentive Fees and Competition in Pension Funds:

Evidence from a Regulatory Experiment

Assaf Hamdani, Eugene Kandel, Yevgeny Mugerman and Yishay Yafeh

Abstract

Concerned with excessive risk taking, regulators worldwide generally prohibit private pension funds from charging performance-based fees. Instead, the premise underlying the regulation of private pension schemes (and other retail-oriented funds) is that competition among fund managers should provide them with the adequate incentives to make investment decisions that would serve their clients’ long-term interests. Using a regulatory experiment from Israel, we compare the effects of incentive fees and competition on the performance of three exogenously-given types of long-term savings schemes operated by the same management companies: (i) funds with performance-based fees, facing no competition; (ii) funds with AUM-based fees, facing low competitive pressure; and (iii) funds with AUM-based fees, operating in a highly competitive environment. Our main result is that funds with performance-based fees exhibit significantly higher risk-adjusted returns than other funds, but are not necessarily riskier (that depends on the measure of risk used). By contrast, we find that competitive pressure leads to poor performance, and conclude that incentives and competition are not perfect substitutes in the retirement savings industry. Our analysis suggests that the pervasive regulatory restrictions on the use of performance-based fees in pension fund management may be costly for savers in the long-run and should be reconsidered.

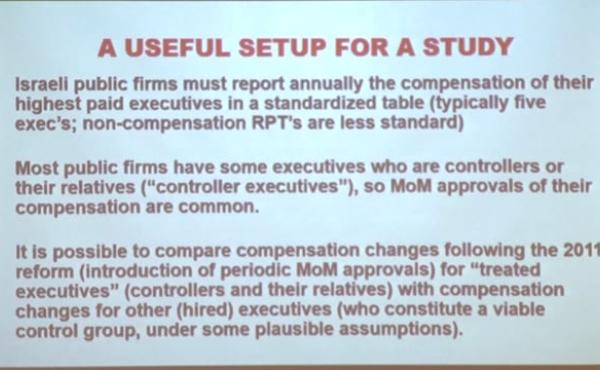

Empowering Minority Shareholders and Executive Compensation:

Evidence from a Natural Experiment

Jesse Fried, Ehud Kamar, and Yishay Yafeh

Abstract

We use a recent regulatory change in Israel to examine the efficacy of minority shareholder approval. In 2011, the level of minority shareholder support required for approving related party transactions, including executive compensation paid to controlling shareholders or to their relatives, increased from a third to a majority of the minority votes cast, and a new rule required renewal of this approval every three years. Comparing changes in compensation following approvals before and after the reform, we find that only the new type of approval constrains compensation, and that this effect is present only when the firm does not choose the timing of the vote. This finding has implications for the design of shareholder voting mechanisms not only on executive compensation but also on other corporate decisions.