The ECGI blog is kindly supported by

Who cares about Diversity?

Authors

The recent study by Gider, Renneboog, and Zhang (2025) examines who actually cares about corporate diversity, equity, and inclusion (DEI) by analyzing stakeholder responses to discrimination litigation. The research investigates whether discrimination lawsuits—related to gender, race, disability, age, and appearance—significantly impact various corporate stakeholders, from financial markets to employees, consumers, and government entities.

The authors analyze 5,586 discrimination lawsuits affecting U.S. public companies between 2001 and 2021. Their methodology uses these litigation events as "shocks" to corporate DEI quality, enabling them to assess how different stakeholders respond to these incidents. They first validate that these events represent genuine DEI shocks by demonstrating that both news coverage and ESG ratings significantly change following litigation filings.

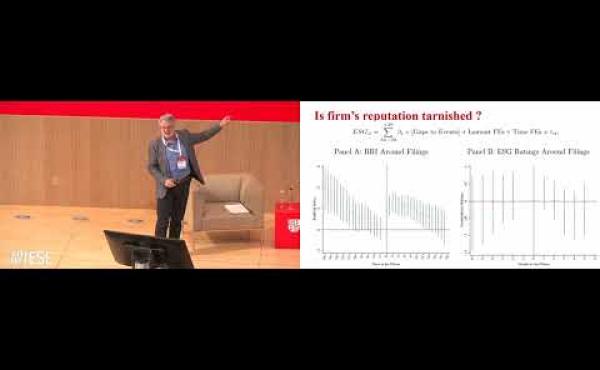

Surprisingly, the study finds no significant stock or bond price reactions to discrimination litigation announcements, despite their visibility in media and among rating agencies. While some institutional investors, particularly mutual funds, temporarily reduce their ownership stakes in sued firms, this selling pressure is quickly absorbed by other shareholders, leaving stock prices largely unchanged.

The research reveals interesting patterns in non-financial stakeholder responses. General employees show little reaction to DEI incidents at their employers, as measured by employee ratings on platforms like Indeed. However, highly skilled employees involved in innovation and R&D demonstrate a different pattern—they are more likely to leave following discrimination litigation. This effect is particularly pronounced for female researchers after gender-related discrimination cases, who show a 24% increase in departure rate in the three months following such filings.

Regarding business relationships, the study finds that supply chain partners (corporate customers and suppliers) show no significant changes in their dealings with firms facing discrimination lawsuits. Similarly, government entities at federal, state, and local levels maintain consistent levels of subsidies, tax benefits, and favorable loan terms to sued companies.

Consumer behavior, analyzed through household-level scanner data for retail products, reveals a modest short-term decline in sales for brands owned by litigated firms—approximately 1% of average monthly household consumption in the three months following litigation. However, this effect dissipates after three months, suggesting consumers have short memories regarding corporate DEI incidents. Interestingly, specific demographic groups show stronger reactions: older consumers, urban households, white households, and those living in counties with predominantly Democratic voters or Catholic populations reduce their consumption more significantly.

While external stakeholders show limited sustained reactions, the study finds evidence of internal corporate governance adjustments. Firms increase board diversity by appointing more female and minority directors following discrimination incidents, suggesting that companies may be taking preventive measures against future litigation.

The authors acknowledge that their study may underestimate the full impact of DEI issues since many discrimination cases are settled confidentially before reaching litigation. Nevertheless, the breadth of their sample allows for robust conclusions about stakeholder reactions to public DEI controversies.

Overall, this comprehensive analysis suggests that while discrimination litigation triggers some reactions—particularly among certain consumers, skilled employees, and in internal governance structures—its aggregate effect on firm value and stakeholder relationships remains limited. The findings contribute to our understanding of how DEI concerns translate into concrete stakeholder behaviors and highlight the differential responses across stakeholder groups.

_______________

Luc Renneboog is a Professor of Corporate Finance at Tilburg University and an ECGI Research Member.

The ECGI does not, consistent with its constitutional purpose, have a view or opinion. If you wish to respond to this article, you can submit a blog article or 'letter to the editor' by clicking here.