K-pop and meme stock

Issue 6 | September 2023

Greetings from Brussels,

I hope that you enjoyed a relaxing summer break (at least for those of you in the northern hemisphere!). To make the back-to-work transition somewhat light and entertaining, this newsletter discusses K-pop and meme stocks. What do these pop-cultural trends have to do with corporate governance and responsible capitalism you may ask. Let’s see, shall we?

In June ECGI organised the annual Global Corporate Governance Colloquium in Seoul , followed by a special series of the blog, focusing on Asia . The different blog contributions cover a wide array of topics, ranging from Asian governments that are spearheading the ESG movement to concrete examples like Japan’s MSCI Empowering Women Index, whose quasi-tournament-like structure led to a significant increase in women in the workforce.

One blogpost I particularly enjoyed discusses a case of shareholder activism in the K-pop (Korean pop music) industry. Last year the prominent K-pop production company SM Entertainment was targeted by the activist fund Align Partners. With just a 1.1% stake in the company the activist successfully campaigned to terminate the ‘tunneling practices’ of the firm’s founder Mr. Lee, who had reaped substantial portions of the annual profits.

In the past, shareholder activism held little relevance for Korean enterprises. Controlling shareholders in most listed firms hindered activists, and Korean asset managers, tied into business relationships with major conglomerates, typically sided with the controlling shareholder. Korea is not an outlier in this, as controlling shareholders are prominent throughout most Asian countries, (and, indeed, in most markets globally, apart from the Anglo American world).

Nevertheless, Align Partners appears to have sparked a rise in shareholder activism. This recent activism coincides with a surge in the number of Korean retail investors, from 6.14 million in 2019 to 13.74 million in 2021, and new technology, enabling the delegation of voting rights online. Seemingly, retail investors are eager to use their newly acquired shareholder rights when prominent companies and their favourite K-pop idols are involved.

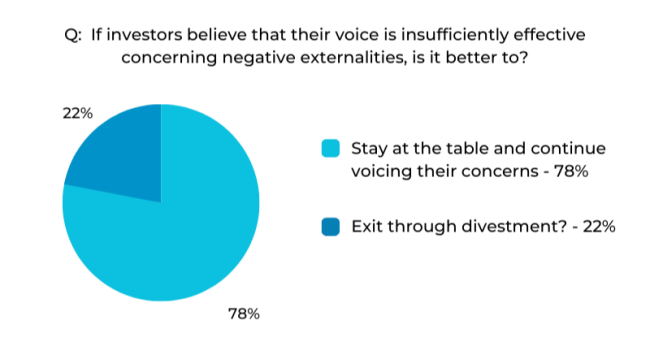

Observing this blend of new technologies, a new generation of investors and a growing discontent with societal issues, the authors of ‘Meme Corporate Governance ’ ask: ‘Can retail investors revolutionise corporate governance and make public companies more responsive to social concerns?’

They find that the phenomenon of ‘meme stock’ investing rose when online brokers offered commission-free trading and social media platforms allowed retail investors to strategise and coordinate targeted ‘buy’ campaigns. Could this coordinated investment behaviour also translate to coordinated and improved shareholder engagement and corporate governance? So far this does not seem to be the case. In fact, the targeted firms experienced a substantial decrease in shareholder voting after the influx of retail investors. Nor did director independence, board gender diversity, ESG scores or capital and R&D expenditures improve. Even the investors who have stayed loyal to the companies over years have not increased their involvement.

The authors offer a number of explanations for their findings. Commission-free investments presumably don’t attract the types of investors willing to bear the transaction costs that come with submitting shareholder proposals and voting. While the payoff from a ‘meme trade’ can be realised rather quickly, shareholder voting is more tedious, results are not imminent and the individual may experience that their vote does not really make a difference. Technology has significantly reduced the participation cost associated with becoming a shareholder, yet being active and engaged in the investee company is inherently information-intensive and therefore cost-intensive. Retail investors may furthermore lack the necessary skills to influence and pressure the management.

With capital markets in Asia and Europe increasingly opening up to retail investors, there seems to be a lack of vision as to which role retail investors could play as shareholders. The self-organisation of retail investors is so far largely limited to trading, and does not noticeably stretch to shareholder participation. New technology may change this in the coming years, allowing investors to easily coordinate, share and filter information and vote, all in an app.

Could this be the beginning of a revolution in shareholder democracy?

The power of the masses does hold a certain fascination. The K-pop fans that got involved in the corporate governance of SM Entertainment have previously campaigned for the reduction of streaming platforms’ carbon emissions and disrupted a Trump rally. Taylor Swift fans’ outrage about Ticketmaster led to a Senate hearing and antitrust investigations and the eight ‘meme companies’ most hyped up by retail investors did raise $5 billion in the past two years.

As impressive as these joint efforts are, I believe they will remain outliers for now. Shareholder engagement, voting and participation can be a tedious and oftentimes boring process. Coordinated shareholder activism may increase around contentious issues , but not every shareholder meeting will turn into a spectacle.

As always, I am curious to hear your thoughts.

Cordially yours,

Marleen

MINI POLL...

Q: Where do you see the future role of retail investors and

shareholder participation?

A) It will remain a niche phenomenon with both capital markets and retail investors vulnerable to mutual exploitation.

or

B) Technology will facilitate both investment and engagement, establishing a useful connection between citizens and businesses.

Marleen Och is a PhD researcher at KU Leuven, Belgium.

She works in the field of sustainable finance and corporate governance, writing about shareholder engagement and sustainability.

Please feel free to get in touch, share your thoughts and let us know how we're doing, email Marleen.Och@ecgi.org and follow us on Twitter at @ecgiorg