Global Corporate Sustainability Report

The Organisation for Economic Co-operation and Development (OECD) has released a new report on the global landscape of corporate sustainability policies and practices. The analysis is based on a recently developed sustainability dataset, which covers over 14 000 companies listed on 83 markets with a total market capitalisation of USD 90 trillion. The report examines the evolving landscape of corporate sustainability practices and some of the most relevant recent regulatory developments. The recently revised G20/OECD Principles of Corporate Governance are the key reference for the issues covered in the report, including recommendations on sustainability-related disclosure, the dialogue between a company and its shareholders, the board of directors' responsibilities, and stakeholders' interests.

Access to material sustainability information is crucial for market efficiency and investor protection. Across OECD, G20, and FSB jurisdictions, a specific provision, requirement, or recommendation has been established regarding sustainability-related disclosure, at least for large listed companies. Nevertheless, even where sustainability-related disclosure is not mandatory, many companies have been reporting on sustainability risks and opportunities.

Globally, almost 9 600 listed companies disclosed sustainability‑related information in 2022 or later. The companies that disclosed sustainability-related information represent 86% of the global market capitalisation.

Disclosure of sustainability-related information by listed companies in 2022

86% of companies by market capitalisation disclose sustainable-related information globally

Source: OECD (2024), Global Corporate Sustainability Report 2024, OECD Publishing, Paris, https://doi.org/10.1787/8416b635-en; OECD Corporate Sustainability dataset, LSEG, Bloomberg.

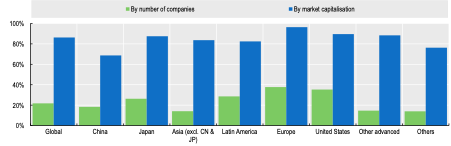

With growing awareness and new regulatory developments related to the climate, the interest of investors in companies’ greenhouse gas (GHG) emissions has risen sharply. Implementing a reporting system is the first critical step in reducing GHG emissions. This involves accurately measuring and tracking scope 1 (direct), scope 2 (indirect through energy use) and scope 3 (supply chain and financed entities) emissions. Globally, 6 308 companies representing 77% of market capitalisation disclosed scope 1 and scope 2 GHG emissions in 2022, ranging from 43% of companies by market capitalisation in the People’s Republic of China (China) to 92% in Europe. As expected, companies report scope 3 GHG emissions less frequently.

Disclosure of GHG emissions by listed companies in 2022

While Europe leads in scope 1 and 2 GHG emissions disclosure, less than two-thirds of companies disclose scope 3 GHG emissions globally

Source: OECD (2024), Global Corporate Sustainability Report 2024, OECD Publishing, Paris, https://doi.org/10.1787/8416b635-en; OECD Corporate Sustainability dataset, LSEG, Bloomberg.

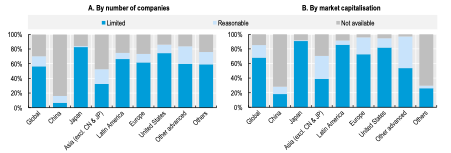

An independent assurance may ensure the transparency and reliability of sustainability‑related information, increasing investors’ confidence and facilitating comparisons between companies. Globally, external service providers assure the sustainability reports of two-thirds of the companies disclosing sustainability information by market capitalisation. However, external assurance over sustainability information is or will become mandatory only in some large markets, such as Europe and India. In 2022, a “limited” level of assurance was considerably more common than a “reasonable” one.

Level of sustainability reports assurance in 2022

Reasonable assurance of sustainability reports remains uncommon

Source: OECD (2024), Global Corporate Sustainability Report 2024, OECD Publishing, Paris, https://doi.org/10.1787/8416b635-en; OECD Corporate Sustainability dataset, LSEG, Bloomberg.

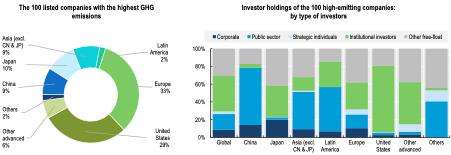

An analysis of the top 100 listed companies with the highest disclosed GHG emissions reveals that institutional investors hold the largest share globally, at 41%, in these companies. At the same time, the public sector plays a significant role in China, holding 64% of equity, and in Latin America, holding 50%. Europe shows a more diversified investor base. This underscores the crucial role of corporate governance frameworks in encouraging shareholders’ engagement with their investee companies.

100 listed companies with the highest GHG emissions

Institutional investors hold the largest equity portion (41%) in the highest-emitting

100 companies

Source: OECD (2024), Global Corporate Sustainability Report 2024, OECD Publishing, Paris, https://doi.org/10.1787/8416b635-en; OECD Capital Market Series dataset, OECD Corporate Sustainability dataset, FactSet, LSEG, Bloomberg.

In line with the G20/OECD Principles of Corporate Governance, the Global Corporate Sustainability Report 2024 brings several key policy messages, including:

- Sustainability-related disclosure frameworks may need to be flexible about the existing capacities of companies.

- Standard‑setters should work together to make their standards as interoperable as feasible, reducing the costs for companies that must disclose sustainability-related information according to different standards.

- Regulators in jurisdictions where voluntary assurance is a common practice may consider requiring large listed companies to obtain assurance over their sustainability-related information.

- Wherever high-quality assurance for all disclosed sustainability-related information might not be possible or is too costly, jurisdictions may require companies to obtain assurance over specific sustainability-related disclosures, such as GHG emissions.

- Investors and regulators may need to pay special attention to whether executives can choose to hire the company’s external auditor to provide sustainability-related assurance without the approval of the board, the audit committee or shareholders.

- Whenever included in a company’s reduction targets, market participants and relevant stakeholders should consider ways to encourage the disclosure of scope 3 GHG emissions.

-------------------

You may download the OECD Global Corporate Sustainability Report here.

By Caio de Oliveira, Adriana De La Cruz and Valentina Cociancich, OECD.

Caio de Oliveira is the team leader for sustainable finance, and Adriana De La Cruz and Valentina Cociancich are policy analysts in the Capital Markets and Financial Institutions Division within Directorate for Financial and Enterprise Affairs of the Organisation for Economic Co-operation and Development (OECD). This article is based on an OECD report launched on March 14, 2024. This article should not be reported as representing the official views of the OECD or of its member countries. The opinions expressed and arguments employed are those of the authors.